The Strategic Pivot: A Guide to Navigating Digital Banking Replacement for Modern Credit Unions

Digital banking is no longer a differentiator. It is now the primary way members engage with their financial institution. For credit unions across North America, upgrading digital banking platforms is no longer optional. It is a strategic imperative driven by evolving member expectations, increasing cybersecurity threats, and intensifying competition from fintechs and digital-first banks.

However, modernization carries its own risks. Poorly executed upgrades can disrupt member experiences, introduce compliance gaps, and create long-term architectural constraints. The goal is not simply to “modernize,” but to do so in a way that is incremental, resilient, and aligned with both regulatory requirements and long-term business strategy.

This article outlines best practices to help credit unions navigate digital banking upgrades effectively.

Why Upgrading Now Is Non-Negotiable

Member expectations have fundamentally shifted. Users now expect seamless, mobile-first experiences, real-time transactions, and personalized financial insights. At the same time, fintech entrants continue to raise the bar with intuitive interfaces and rapid feature delivery.

Internally, many credit unions are constrained by legacy systems, monolithic architectures, batch-based processing, and tightly coupled integrations that limit agility. Layer on increasing regulatory scrutiny and the rising sophistication of cyber threats, and the need for modernization becomes urgent.

Digital banking upgrades are no longer just IT initiatives; rather, they are core to member retention, growth, and operational resilience.

Common Pitfalls in Digital Banking Modernization

Before outlining best practices, it is critical to understand where institutions often go wrong.

A common misstep is the “big bang” replacement approach, where organizations attempt to swap out entire platforms in a single initiative. This introduces significant operational risk and often leads to delays or failures.

Another frequent issue is underestimating dependencies on core banking systems. Many digital channels are deeply intertwined with legacy cores, making changes more complex than anticipated.

Credit unions also risk focusing too heavily on backend transformation while neglecting the member experience during the transition. Even temporary disruptions can erode trust.

Finally, vendor lock-in remains a persistent challenge. Selecting platforms without sufficient openness or extensibility can limit future innovation.

Guiding Principles for Modernization

Successful digital banking upgrades are grounded in a set of architectural and operational principles.

Member-Centric Design

Modernization should start with member journeys, not systems. Every architectural decision should support seamless, consistent experiences across mobile, web, and assisted channels such as branches and contact centers.

API-First and Composable Architecture

An API-first approach decouples digital channels from backend systems, enabling faster innovation and easier integration with third-party services. Composable architecture (a modular design approach that builds software systems by assembling independent, interchangeable components using APIs) allows credit unions to evolve capabilities incrementally rather than relying on monolithic platforms.

Incremental Modernization

Rather than replacing entire systems at once, leading institutions adopt incremental strategies by gradually introducing new components while retiring legacy ones. This reduces risk and allows continuous value delivery.

Cloud-Native Infrastructure

Cloud-native approaches provide scalability, resilience, and operational efficiency. When implemented correctly, they also support regulatory requirements around availability, disaster recovery, and auditability.

Security by Design

Security must be embedded at every layer. This includes zero-trust architectures, strong authentication mechanisms such as multi-factor authentication and biometrics, and continuous monitoring for threats.

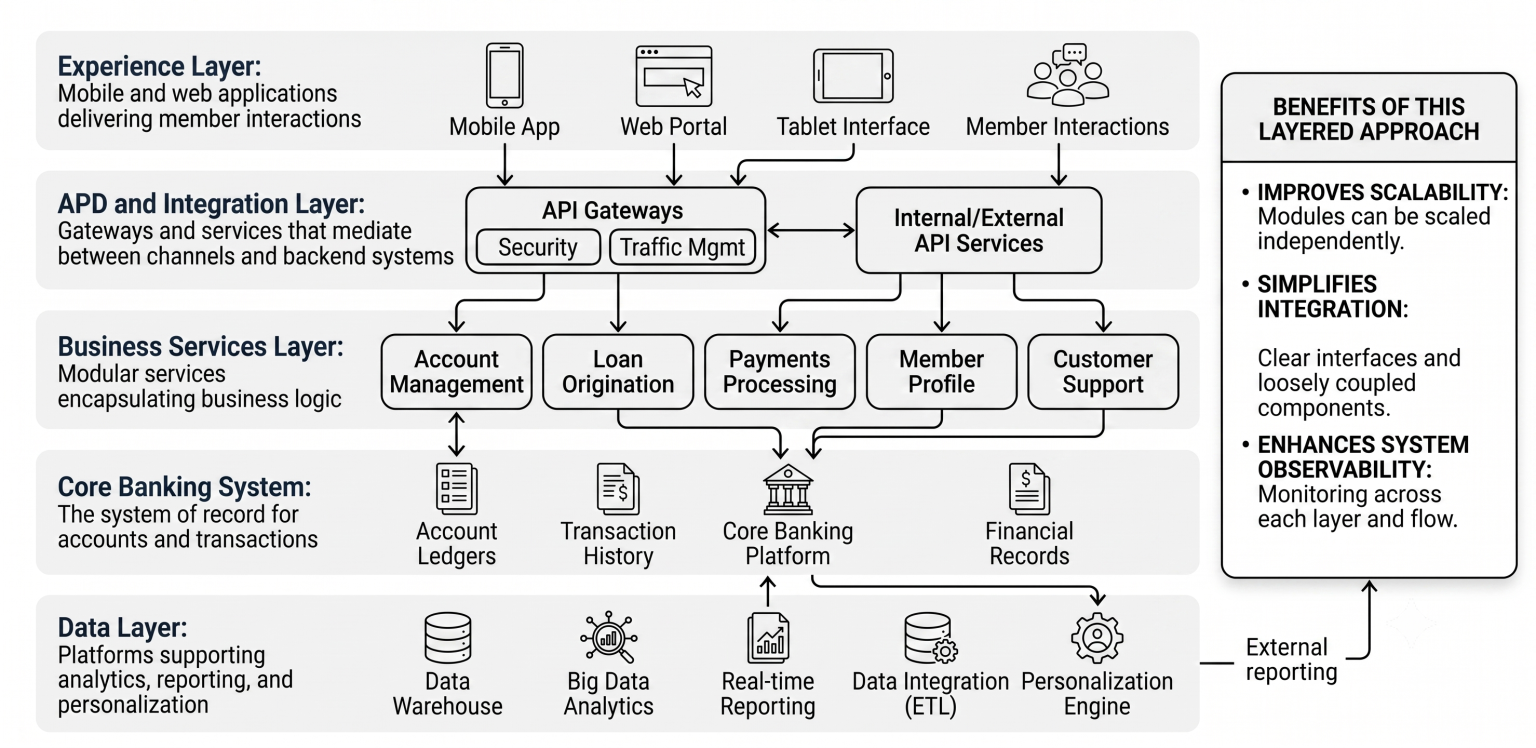

A High-Level Architecture Blueprint

A modern digital banking architecture typically consists of several loosely coupled layers:

- Experience Layer: Mobile and web applications delivering member interactions

- API and Integration Layer: Gateways and services that mediate between channels and backend systems

- Business Services Layer: Modular services encapsulating business logic

- Core Banking System: The system of record for accounts and transactions

- Data Layer: Platforms supporting analytics, reporting, and personalization

This layered approach improves scalability, simplifies integration, and enhances system observability.

Regulatory and Compliance Considerations

For credit unions, modernization must align with a complex regulatory environment.

Data privacy regulations in both Canada (PIPEDA, Personal Information Protection and Electronic Documents Act) and the United States GLBA (Gramm-Leach-Bliley Act 1999, also known as the Financial Services Modernization Act, 1999) require careful handling of member information, including data residency and consent management. Systems must also support auditability, ensuring that all transactions and changes are traceable.

Third-party risk management is another critical area. As institutions adopt more vendor solutions and fintech integrations, they must ensure those partners meet security and compliance standards.

Business continuity and disaster recovery capabilities are also non-negotiable. Regulators expect institutions to demonstrate resilience under various failure scenarios. Some credit unions maintain disaster recovery (DR) environments in geographically separate regions to ensure operational resilience in the event of natural disasters such as earthquakes or flooding.

Accessibility requirements must not be overlooked. Digital platforms should comply with recognized accessibility standards such as the Accessible Canada Act (ACA) and the Americans with Disabilities Act (ADA) to ensure inclusive member experiences.

Build vs. Buy: Finding the Right Balance

A key strategic decision in any modernization effort is determining what to build internally versus what to procure from vendors.

Commodity capabilities (such as card issuing and transaction processing, digital onboarding and KYC/AML verification, fraud detection services, payments processing, and identity verification) are often best sourced from established providers. These solutions benefit from scale, compliance maturity, and ongoing updates.

However, member-facing experiences and differentiation layers are often better developed in-house or through highly customizable platforms. This allows credit unions to tailor services to their unique member base.

Regardless of approach, openness is critical. Platforms should offer robust APIs and avoid proprietary constraints that limit future flexibility.

Data Strategy and Personalization

Data is central to modern digital banking. Credit unions should aim to establish a unified view of the member, consolidating data across systems. Real-time data access is increasingly important, enabling timely insights and interactions.

Personalization can drive meaningful engagement through targeted offers (such as lifecycle-based lending offers and transaction-driven offers), proactive alerts, and financial wellness tools. However, these capabilities depend on strong data governance, quality, and security practices.

DevOps and Delivery

Modernization is not just about architecture; it is also about how software is delivered.

Adopting DevOps best practices enables faster and safer releases. Continuous integration and continuous deployment (CI/CD) pipelines automate build, test, and deployment processes.

Automated testing across functional, integration, and security dimensions reduces defects and improves confidence in releases. Infrastructure as Code (IaC) ensures consistency and repeatability in environment provisioning.

Observability is equally important. Comprehensive logging, metrics, and tracing allow teams to detect and resolve issues quickly.

Feature flags can further reduce risk by enabling controlled rollouts and rapid rollback if needed.

Change Management and Organizational Alignment

Technology alone does not guarantee success. Digital banking upgrades require alignment across business, IT, and compliance teams. Cross-functional collaboration ensures that solutions meet operational, regulatory, and member needs.

Training and internal adoption are critical. All member-facing staff and contact center agents must understand new systems and processes to support members effectively.

Clear communication with members is also essential. Setting expectations and providing guidance during transitions can mitigate frustration and build trust.

Migration Strategy and Roadmap

A structured migration approach is key to minimizing disruption.

Start with a thorough assessment of the current environment, including system dependencies and risk areas. Define a clear target state aligned with business goals.

Prioritize initiatives based on impact and complexity, focusing on high-value, low-risk opportunities first. Phased rollouts allow for testing and refinement. For example, it can begin with employees to ensure internal readiness, followed by member ambassadors for feedback and validation, and conclude with a full rollout to all members.

Parallel runs and rollback strategies provide safety nets during transitions. At each stage, track key performance indicators such as system uptime, member adoption, and satisfaction.

Key Takeaways

- Digital banking modernization is a strategic necessity, not a discretionary project

- Incremental approaches reduce risk and enable continuous value delivery

- Architecture decisions should prioritize flexibility, scalability, and integration

- Security and compliance must be embedded at the earliest stages

- Member experience should remain the central focus throughout the journey

Moving Forward

For credit unions, the path to modern digital banking is both challenging and achievable. The most successful institutions take a pragmatic approach by balancing innovation with risk management and long-term vision with incremental execution.

The first step is not a full transformation, but a clear assessment of where you are today and where you need to go. From there, targeted initiatives can begin delivering value while laying the foundation for future growth.